It is not the legal successor of the reorganized company for tax obligations.

Secondly, there is no universal succession of civil claims, that is, the transfer of all rights and all obligations from the old company to the new one does not occur. The decision on what to transfer and what to leave is made by the participants of the reorganized legal entity.

Both features allow the use of "allocation" to isolate the assets of a business, by transferring to a new entity. It is important that such separation does not entail tax consequences for either the transferring or receiving party.

In addition, the selection allows you to separate the core and auxiliary areas of business for different legal entities. This protects independent business lines from each other's risks in the future.

As a result of the reorganization, a new legal entity is created that can apply any taxation system, including the simplified tax system. Thus, it becomes possible to pay income tax at a reduced rate.

We believe that it will not surprise anyone that the presence of such pleasant bonuses causes close interest of regulatory authorities in the selection procedures.

VAT recovery and reasonable economic purpose

Main claims tax authorities pursuing the allocation is the restoration of VAT. They usually occur in the case of "withdrawal" real estate from the reorganized company after deductions have been granted to it for the production costs of construction and the subsequent transfer of such real estate to the assignee applying the simplified tax system. Recall tax code in paragraph 8 of Art. 162.1, sub. 2 p. 3 art. 170 directly indicates that there is no need to restore VAT in such a situation.

In general, no one argues with this norm, there are no complaints about the reorganization itself. Questions arise about the transfer of property to special. mode. The tax authorities see such actions as a scheme aimed at obtaining unjustified tax benefits in the form of unreasonably received VAT deductions.

The essence of the claims is that the former owner received the deduction, but did not use the object in VAT activities, which means that he will not pay tax on the sale. Total - the budget at a loss. It is not surprising that taxpayers are taxed additionally.

The result of challenging the decision of the IFTS in the above situation largely depends on the presence of a reasonable economic (business) goal in the actions of the taxpayer. If there is none, there is a high probability that the inspectorate will win the dispute.

Given: the company is building a shopping and entertainment center, while declaring VAT deductions. Upon completion of construction, the company announces a reorganization in the form of the allocation of two legal entities. The successors, among other things, transfer ownership of the constructed mall. At the same time, one of the successors in 2 months goes to the simplified tax system. The shopping and entertainment center building is further leased to third parties without VAT.

Conclusion of the tax authority: coordination of actions for the consistent reorganization of legal entities in order to evade the obligation to restore VAT in connection with the transition to the simplified tax system.

The taxpayer refuted the conclusion, pointing out that the reorganization was aimed at dividing activities into areas: both the operation and maintenance of networks. It is important that the separation was necessary in the first place, in view of the fact that activities in the energy market are subject to regulation, and the harmonization of tariffs for energy transmission requires separate accounting costs for the specified type of activity in the company, which, if there were, among other things, accounting for operations related to the construction of a shopping and entertainment center, was practically impossible.

It is noteworthy that this argument was accepted by the courts of three instances, in connection with which the taxpayer managed to avoid additional charges in the amount of about 24 million rubles, as well as the payment of a fine.

Reorganization errors

If the declared business purpose is subtle, then the claims of the tax authorities may be supported in court. Let's illustrate again with an example.

Given: two companies LLC "Keeper of Assets" on the OSN and LLC "Operating Company" on the USN. The first owns property - a restaurant. The second one rents this property and uses it for its intended purpose. It is important that the premises themselves were acquired quite recently and in the tax period preceding the events described below, a VAT refund was received from the budget.

Business owners came up with a simple plan: to transfer assets to the simplified tax system, avoiding the restoration of VAT. To do this, the owner decided to reorganize in the form of a spin-off.

(1) Separation of Promezhutok LLC with the transfer of real estate to it. Recall that the decision on the allocation was made in the next quarter after the confirmation of the VAT deduction and receipt of reimbursement from the budget;

(2) After registration, Promezhutok LLC applies the OSN, but from January 1 of the next year it switches to the USN. At the same time, the same application is submitted by the original company - "Keeper", which got rid of valuable property;

(3) A few months later, the procedure for merging LLC Promezhutok with the Operating Company (restaurant) begins.

The tax authority did not like such actions. In his opinion, Promezhutok LLC should have restored VAT. And since the accession was completed by the time the demand was made, the Operating Company was hit.

Consider the taxpayer's mistakes that led to the described result:

First, the reorganization was announced immediately after receiving the VAT deduction. At the same time, the owner of the property did not conduct independent activities, which means that he did not pay VAT on sales to the budget. Conclusion - the property was purchased to receive a deduction. Obviously, the tax authority simply could not allow such a thing.

Secondly, during the allocation, the balance of the distribution of rights and obligations with the assignee was not observed. In this case, according to the separation balance sheet, the new Company received a restaurant complex, but no obligations were transferred to it.

Third, the business purpose of the reorganization. In this case, he tried to prove that all the actions he had taken were aimed solely at reducing the cost of the operating company to pay rent. In support of the stated business goal, they even provided an audit report.

However, against the background of the interdependence of the reorganized entities and other mistakes of the taxpayer, such a goal did not suit the courts.

Fourth, despite the fact that the case is related to the reorganization, the claims of the tax authority are based on the next step - the transition to the simplified tax system.

The courts have explicitly stated that the reorganization itself does not necessitate the restoration of VAT. However, the purpose of the allocation in this case is to evade the obligation to restore VAT in connection with the subsequent transition of the taxpayer to special. mode. In other words, the taxpayer previously carried out a reorganization in order to withdraw property and create a formal opportunity not to restore the tax accepted for deduction.

The implications of the case are clear. To avoid adverse tax consequences:

it is impossible to reorganize with the transfer of fixed assets immediately after receiving deductions. Wait a significant amount of time. A few years after the acquisition of the property, the tax authority will have no reason to refer to the lack of intention to conduct VAT-taxable activities;

a reorganization cannot be carried out without a clear business purpose. You should not take the allocation as a way to recover VAT and not pay it on future activities. Reorganization primarily serves as a business optimization tool;

it is impossible to transfer a reorganized company to a simplified taxation system. Despite the fact that she no longer owns the property, the tax authority will ask to restore VAT;

need to plan ahead. Do not provoke the tax authority with the subsequent transition of the new company to the simplified tax system. Dedicated legal entity person must apply special mode since its inception.

Analysis of the current judicial practice allows you to derive a number of additional rules. Of course, the decision to follow them or not is an independent choice, but we recommend listening.

Do not make sudden movements after the end of the selection

The result of the reorganization in the form of a spin-off must be self-sufficient and final. If this is one of the “preparatory stages” for something, then the business purpose of the spin-off cannot be justified.

For example, the sale of property by the successor to the simplified tax system immediately after the reorganization will raise a fair question that the sole purpose of the allocation was to pay tax when selling at reduced rates. There was no intention to conduct independent activities.

The tax authorities and the court will come to a similar conclusion in the event of a repeated reorganization after the purchase of the next object and the acceptance of VAT for deduction. That is, it is impossible to carry out the selection regularly.

The successor must conduct independent activities

At the same time, the transfer of property for rent from the allocated (new) organization to the company from which it was allocated will not help. Other counterparties are important cash flows and availability of employees. Accordingly, if the company has one tenant and one employee, and the rent is not paid regularly, prove that the whole thing - real business will not work .

Economic efficiency of reorganization

The position of the taxpayer will be strengthened by the achievement economic effect from the reorganization. For example, increasing profitability after the separation of an independent business area. And, on the contrary, a clear deterioration in the “economy” will not play in favor of the taxpayer:

after the transfer of fixed assets to the assignee, the taxpayer leases them. At the same time, the amount of the rent is many times higher than the depreciation deductions;

all costs of maintaining the property are still borne by the taxpayer as a tenant;

cash in the form of overpriced rent transferred to the lessor is then re-transferred to the taxpayer (tenant) or other related companies in the form of loans.

In the present case, the court held that the sole purpose of the allocation was to overstate the former owner's expenses in the form of rental payments. At the same time, the actual business processes did not change, the company continued to use “its” property.

Joint and several liability of the "new" company

The general rule establishes that the separated legal entity is not liable for the obligations (including tax) of the predecessor company. However, if certain conditions are met, joint and several liability arises between the new and old organizations.

In terms of tax liabilities, these are: the inability to pay taxes and the focus of the reorganization on tax evasion. In terms of civil liability: the deed of transfer does not allow to determine the successor to the obligation, or the assets and liabilities are distributed unfairly.

It is important that in order to attract a person as a joint and several debtor, it is necessary to go to court, which means that the tax authority or another creditor must prove the existence of the indicated conditions.

Tax liabilities

The inability to pay taxes is proved quite simply. In the course of measures to collect tax debts from the main debtor, the inspection reveals "0" on the current account. After that, it makes a decision on the collection of debt at the expense of property, which is sent to the bailiffs - executors. The latter, in turn, establish the fact that the debtor has no property, in connection with which the enforcement proceedings are terminated.

The next task is to prove that the reorganization was aimed at tax evasion. To do this, the inspectorate, in particular, may refer to the facts of the taxpayer performing actions aimed at concealing Money, due to which it was possible to repay the debt to the budget. For example, if a taxpayer, in the presence of a card index in a bank account, asks customers to pay directly to his counterparties, or during the reorganization, all liquid assets were transferred to the successor.

It is important that the successor can only be involved in paying tax debts for the three years preceding the spin-off. Three years after the end of the allocation, you can sleep peacefully.

Claims of other creditors

Bringing a spin-off company to joint and several liability in civil cases depends on the presence of one of the two above-mentioned conditions. At the same time, in practice, the solution of the problem has a lot of features. Here are some findings from jurisprudence:

(1) With regard to unfair distribution

It is important to approach this feature reasonably, that is, the fulfillment of the obligation must be adequate. Obviously, the transfer of 100 rubles to the creditor once a month will not change the picture.(2) With the impossibility of determining the successor under the deed of transfer, in general, everything is clear: if the obligation does not appear in the deed, both are responsible. However, there are nuances in this part.

Firstly, the preparation of the transfer act must be approached scrupulously. So, for example, it is desirable to name the counterparties and make a reference to specific obligations, including specifying the details of the contracts and the balance for the period the act was drawn up.

In practice, generalizations are often encountered, for example: "... what is not indicated in the act remains with the reorganized legal entity ...". In general, such an indication is permissible, if only because, in accordance with part 1 of Art. 59 of the Civil Code of the Russian Federation, the transfer act should establish the procedure for determining succession in the event of the emergence, change or termination of obligations of the legal entity being reorganized, which may occur after the date of approval of the transfer act.

Secondly, situations concerning obligations that arose after the reorganization stand apart. In this case, it is necessary to analyze the essence of the relationship between the debtor and the creditor.

So, the fulfillment of obligations that arose after the reorganization, but arising from relations that developed before it began, can be assigned to a spin-off (new) company in the event of an unfair distribution of assets and liabilities. An example of such a situation is the recovery of a penalty under a loan agreement.

On the other hand, after the end of the separation procedure and signing of the deed of transfer, the reorganized company continues its activities, during which it independently makes decisions and enters into new relationships with third parties. Accordingly, a spin-off company cannot be a legal successor for obligations arising after the reorganization.

In conclusion, we give the main advice - do not abuse it. It concerns both the use of the tool as a whole and the use of its individual features. Reorganization in the form of separation was not invented to optimize taxes, and even more so it is not a way to "forgive everyone who owes." First of all, it is an opportunity to optimize business, solve entrepreneurial problems.

Let's repeat typical mistakes reorganizations that will allow the tax authority or other creditor to doubt the sincerity of intentions:

the reorganized companies have no clear business purpose, they lease all the property “back”;

the property is transferred immediately after receiving the VAT deduction;

the reorganized company switches to a special tax regime after spin-off;

new company is created in general mode and switches to special later;

the assignee on the simplified tax system sells the property immediately after the reorganization;

sharp increase expenses of the old company for renting property from its own successor;

other facts, based on which there is no transparent economic logic, except for the desire to reduce taxes.

1. See letter of the Ministry of Finance of the Russian Federation of July 30, 2010 No. 03-07-11 / 323, as well as letter of the Federal Tax Service of Russia of March 14, 2012 No. ED-4-3 / [email protected]

2. That is, the main purpose of the operation should not be tax savings.

4. See, for example, case no. A10-3798/2016.

5. One of the successors received assets that ensure the transmission (transit) of electricity.

6. See case no. A32-2471/2015. Similar conclusions were made in case No. A27-15970/2016

7. See case No. А47-10141/2015

8. See case No. А02-553/2017

9. See case No. А05-9428/2016

10. Joint and several liability is the obligation of several debtors to satisfy the creditor's claim. In this case, the creditor has the right to demand full satisfaction both from all debtors and from one person.

11. See case no. A27-23391/2014

12. See case No. А40-101831/2014

13. See case No. А53-14577/2017

14. See case No. А32-15413/2017

- This is a type of reorganization in which the organization does not cease to exist.

A legal entity is considered reorganized from the moment state registration newly emerged legal entities on the basis of a deed of transfer, which must contain provisions on the succession of all obligations of the reorganized legal entity in relation to all its creditors and debtors, including obligations disputed by the parties, as well as the procedure for determining succession in connection with a change in the type, composition, value of property , the emergence, change, termination of the rights and obligations of the reorganized legal entity, which may occur after the date on which the deed of transfer is drawn up.

When reorganizing by spin-off, one or more legal entities are created, which will be considered newly created as a result of the reorganization.

Procedure reorganization by separation of LLC in the economic sense mediates the division of capital between the founders. In its purest form, it means the creation of a separate society, inheriting certain rights and obligations of the original society, and is aimed at dividing the business. However, in its pure form, it is extremely rare, most often in entrepreneurial activity the procedure for reorganization of an LLC in the form of a spin-off is used for the so-called restructuring of the company's debts, in which certain property and certain obligations are transferred to the spun-off company. THE BASIC PACKAGE OF REORGANIZATION SERVICES IN THE FORM OF ALLOCATION INCLUDES:

- Advising the client on the choice of a suitable organizational and legal form of the newly transformed enterprise; collection and analysis of documents

- Package preparation required documents for enterprise reorganization

- Making a seal

- Filing an announcement in the Bulletin of State Registration of Legal Entities Registration of documents in MIFTS, PF, FSS, statistics

- Notice to Creditors

The reorganization of an LLC in the form of a spin-off is in practice used to divide the property of one company between its participants. At the stage of such a reorganization, problems may arise, which often lead to litigation. To date, within the framework of disputes related to such a reorganization, the following issues are considered:

- the ratio of the property transferred to the allocated LLC and the actual value of the shares of the participants transferred to the allocated company

- consequences of the evasion of the separated LLC from the state registration of the transfer of ownership of the property transferred to it

- joint and several liability of companies in case of reorganization in the form of spin-off

When one or more organizations are separated from a legal entity, a part of the rights and obligations of the legal entity reorganized in the form of separation is transferred to each of them in accordance with the deed of transfer.

The transfer agreement is approved by the founders of the legal entity or the body that made the decision on the reorganization, and is submitted together with the constituent documents for state registration of the newly emerged legal entity. Failure to submit a deed of transfer along with the constituent documents, as well as the absence of a provision in it on succession for the obligations of a reorganized legal entity, is the basis for refusing state registration of a newly emerged legal entity.

If the deed of transfer does not make it possible to determine the legal successor of the reorganized legal entity, the newly established legal entities shall be jointly and severally liable for the obligations of the reorganized legal entity to its creditors.

The issues of separation from an LLC cause a lot of different disputes (judicial), when certain parties for whom this procedure is unprofitable try to challenge it. Documents adopted during the reorganization procedure in the form of separation: decisions of general meetings, deed of transfer - undergo a strict and meticulous check, and often do not withstand it.

Faced with such a complex, multi-component legal procedure, you should contact professionals who understand all the intricacies of the current legislation. AT law firm"Logos" clients can always count on a competent and responsible approach to business and prompt, clear actions.

The reorganization of an LLC in the form of a spin-off implies a kind of spin-off from an LLC that is a donor, an independent company. It is registered as a legal entity, and the company from which this company has separated continues to operate on the same legal basis.

Features of reorganization by allocation

At present spin-off has become the most demanded form of reorganization in Russian business circles. The fact is that its use is a consequence of very common circumstances.

The following main reasons for such a reorganization are noted:

- The parent company has a large debt. In this case, when a new enterprise is created, along with a part of property and other rights, debts are also transferred in full or in part. As a result, the parent company continues to work quietly and make a profit.

- Emergence in the process of company growth of highly specialized workshops or branches. The separation of these divisions as independent legal entities contributes to their further development, speeds up business operations and simplifies Accounting. In this case, cooperation between legal entities becomes more profitable than cooperation of branches within the same legal entity.

- Expansion of the company, leading to the complexity of management and making it difficult for its further growth.

- The emergence of sharp disagreements between the owners.

Reorganization by separation, as opposed to other methods (with the exception of separation), is carried out not only according to the wishes of the LLC owners, but also according to the decision made tax service, antimonopoly committee or judicial authority. All such decisions are made solely on the basis of existing legislation.

And also the fundamental difference of this method of reorganization is that only legal entities belonging to the same organizational and legal form as the parent company can be created during spin-off.

Video: Highlight Reorganization Features

Step-by-step reorganization by allocation method

Reorganization by creating a new legal entity while maintaining the old one, like all other methods of reorganization, is regulated by Art. 51 FZ-14 "On companies with limited liability"dated February 18, 1998, as well as Art. 58 of the Civil Code of the Russian Federation.

Previously, the provisions for the implementation of individual stages of the reorganization were not detailed. As a result of the latest amendments to Law No. 14-FZ, which entered into force on 09/01/2017, reorganization issues are spelled out more carefully.

The essence of the introduced amendments:

- proposals for reorganization are introduced by both the founders and other authorized bodies;

- non-compliance by the responsible persons of the company with the decisions of other authorized bodies on the need for reorganization is allowed to be considered in court;

- the legal document for the transfer of powers is only the deed of transfer, and the submission of the separation balance sheet is not mandatory;

- non-compliance of the charter and other documents with the provisions of the law is the basis for invalidating the reorganization;

- creditors have the right to demand early payment of debts.

The amendments regarding the separation process consist in a clear wording of the succession, presented in paragraph 4 of Art. 58 of the Civil Code of the Russian Federation.

When one or more legal entities are separated from a legal entity, the rights and obligations of the reorganized legal entity are transferred to each of them in accordance with the deed of transfer.

In the process of reorganization by allocation, the following steps can be specified:

- Preliminary stage.

- Performing an inventory.

- Registration of the deed of transfer.

- Bringing questions to the general meeting.

- Notifying tax authorities and creditors of the commencement of the reorganization process.

- Placement of the publication about the reorganization.

- Transfer to the IFTS of a package of documents on the reorganization.

- Checking documents and obtaining registration certificates.

- The final stage.

Only scrupulous observance of the sequence of actions during the reorganization guarantees its successful completion.

preliminary stage

It consists in developing a decision on the method of reorganization at the level of the executive body and the board of directors of the enterprise. Comprehensive consultations are held with lawyers and, if necessary, with the tax service and the antimonopoly committee. At meetings and consultations, the best ways to implement the procedure are determined and persons responsible for preparing the general meeting are appointed. At the preliminary stage, draft decisions are drawn up.

General Extraordinary Meeting

The general meeting is organized by the executive body of the company, as well as at the request of the board of directors, audit commission or at the request of a group of founders, constituting at least 1/10 of the number of participants (clause 2, article 35 of Law No. 14-FZ of February 8, 1998).

The announcement of the planned collegiate meetings is drawn up in free form. Here are the following points:

- the name of the body convening the meeting, or the names of the initiating participants;

- the time and place of the meeting;

- list of proposed issues.

The notice of convening an extraordinary meeting must indicate that the agenda includes the issue of reorganizing the company by separating

This message must be sent in writing to all participants in the enterprise and interested companies. The list of addressees is agreed in advance. At the same time, it is desirable that the addressee confirms the fact of receipt of the notice. Otherwise, an absent participant may manipulate the situation and jeopardize the legitimacy of the meeting. And it is also necessary that the notice of the planned event be made no later than 30 days before the fixed date of its convocation (clause 1, article 36 of the Federal Law No. 14).

The registration of participants must be taken very carefully, since all issues are resolved exclusively by collegial and open voting. To approve the resolution on the reorganization by spin-off, you need to have all 100% of the votes. For value adjustment solutions authorized capital, amendments to the charter, distribution of shares and in other similar cases, it is enough for at least two-thirds of the number of participants in the company to vote.

The following items are on the agenda:

- Reorganization of the company by spin-off.

- The formation of a new society by separating from the present.

- The procedure for the reorganization.

- Distribution of authorized capital.

- The choice of the director of the created enterprise.

- Approval of the charter of the new company.

- Approval of the commission for inventory and for the development of a transfer act.

All decisions are made in the form of protocols. According to the provisions of paragraph 3 of Art. 67.1 of the Civil Code of the Russian Federation, the list of persons present at the meeting and the adopted minutes are certified by a notary. However, in new edition The Civil Code of the Russian Federation states that under certain circumstances it is possible to do without notarization protocol. For example, if the composition of the participants and the text of the protocol are signed by all participants or there are technical possibilities to establish the absolute reliability of the approval of decisions, then notarization of the authenticity of documents is not required. And it will also be legal to certify the decisions of the meeting without notarization, if such a provision is included in the charter of the LLC or adopted unanimously at the general meeting.

Copies of the minutes within a ten-day period after the date of its approval are sent to all participants of the company.

Inventory and registration of the transfer act

An inventory check is a prerequisite for reorganization. The rules for its implementation are regulated by the Methodological Guidelines (Order of the Ministry of Finance of the Russian Federation No. 49 dated 06/13/1995).

It is advisable to coincide with the time of the inventory to coincide with the last reporting period before the date of notification of the tax authorities about the start of the reorganization. Based on the inventory, lists of property and lists of financial obligations are compiled. They are primary accounting documents, on the basis of which a transfer act is drawn up.

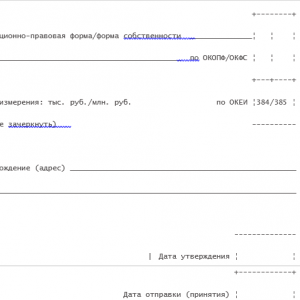

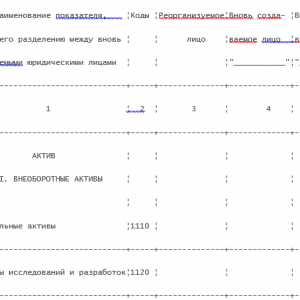

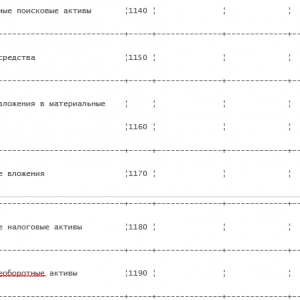

Currently, the legislation only requires the submission of a deed of transfer confirming the succession. Presentation of the separation balance sheet is now optional. However, in practice, the preparation of a deed of transfer is always preceded by painstaking work on the design of a separation balance sheet. There is also no standard form for the separation balance sheet, but as an intermediate document it is very convenient.

The separation balance sheet is handy tool to represent the state of the assets and liabilities of the enterprise

The execution of the deed of transfer in the law is not regulated. Each enterprise has the right to approve its form of act. At the same time, the content of the deed of transfer is clearly regulated by Art. 59 of the Civil Code of the Russian Federation. According to these legislative documents it should contain information about the assets and liabilities remaining in the parent organization and passing to the newly created company or companies.

The deed of transfer shall contain information on the assets and liabilities remaining in the reorganized company and passing to the spin-off company

Modern edition of Art. 59 of the Civil Code of the Russian Federation discloses legal aspects transfer deed.

The deed of transfer must contain provisions on the succession of all obligations of the reorganized legal entity in relation to all its creditors and debtors, including obligations disputed by the parties, as well as the procedure for determining succession in connection with a change in the type, composition, value of property, the emergence, change, termination of rights and obligations of the reorganized legal entity that may occur after the date on which the deed of transfer is drawn up.

Depending on the number of newly created enterprises, the number of columns in the transfer act is drawn up. The principle of drawing up a deed of transfer is the same as in the accounting report of the annual balance sheet. The property of enterprises (each separately and all together) is divided into assets and liabilities, the amounts of which must completely match.

Notification of the tax office and creditors about the start of the reorganization process and press release

About the beginning of the reorganization, a notification is sent to the tax inspectorate on the form P12003 approved by the Federal Tax Service (Order No. ММВ-7-6/ [email protected] dated 25.01.2012).

Form P12003 is allowed to issue:

- handwritten in black ink or black ink in capital letters only;

- in printed version using the font Courier New 18 pixels.

In case of reorganization, the allocation method is filled in:

- Title page. The reason for the reorganization is indicated in it as an allocation, therefore, in paragraph 2, the number “4” is affixed.

On the title page of the form P12003 in the paragraph "Reason" the number "4" is affixed

- Sheet "A". Here you will find information about the company to be reorganized. When allocated, an entry is made only in paragraph 1, where the PSRN and TIN numbers are recorded, as well as the name of the enterprise and its organizational and legal form.

On the first page of sheet "A" of form P12003, data on the legal entity being reorganized are provided

- The first page of sheet "B" - information about the applicant is submitted, which, in case of separation, is also a reorganized company. In paragraph 1 of this page, the details of the company are entered, in paragraph 2 - the position of the person filling out the document (director, other employee, authorized person). Paragraph 3 in the case of reorganization in the form of separation is not filled out, and paragraph 4 indicates the data of the person filling out the document:

- The second page of sheet "B", which, in fact, is a continuation of the first page. Here are indicated:

- Page 3 is completed in the presence of a notary. It is signed by the applicant and one of three ways to obtain documents:

The notification must be submitted no later than three days after the approval of the decision on the reorganization. Together with him, a protocol of the decision to start the reorganization procedure is sent.

In the same manner, notifications are sent to the Pension Fund and the FSS.

Notification of the commencement of the reorganization process must be sent to creditors no later than five days after the decision is made.

After receiving the notification and accompanying documents, the regional tax inspectorate makes an entry in the Unified State Register of Legal Entities about the beginning of the reorganization procedure and informs the applicant of the entry. Having received notice of this entry, the company from which the enterprise is separated is obliged to publish a notice of reorganization in the State Registration Bulletin. This publication must be repeated in a month.

Within five days after the decision of the general meeting, you must inform your creditors about this.

The composition of the documents for the reorganized and newly created enterprises for their transfer to the Federal Tax Service

The law provides for a three-month period from the date of publication of the publication on the reorganization in the Bulletin for the presentation of claims of creditors and the elimination of disagreements. After this time, the company can send documents to the tax office, which are drawn up in the form of two packages:

- Documentation for the registration of a newly created enterprise.

- Documents for the enterprise being reorganized as a result of separation.

The portfolio of documentation for registration of a legal entity that has arisen as a result of spin-off includes the following documents:

- application in the form P12001;

- charter in two copies;

- decision on reorganization in the form of separation (extract from the minutes of the meeting);

- decision on approval of the executive body of the new LLC and approval of the charter;

- a copy of the payment order confirming the payment of the state fee;

- a letter of guarantee confirming the address of the new company;

- deed of transfer;

- copies of two publications in the State Registration Bulletin;

- copies of receipts for sending notices to creditors;

- certificate from the Pension Fund of the Russian Federation on the absence of debt.

An application for state registration of a legal entity created through reorganization is filled out on form P12001 (Appendix No. 1 to the order of the Federal Tax Service of Russia dated January 25, 2012 No. ММВ-7-6 / [email protected]).

Filling out the form in case of selection has its own characteristics:

- Page 1 contains information about the enterprise created as a result of the spin-off. In paragraph 3, the number "4" is affixed - selection.

- On page 2, in paragraph 4, the number of participants in the company being created is indicated.

- Sheet "B" contains information about the participant of the company, which is a legal entity. A separate page is filled out for each such participant.

- If there are individuals among the participants, then the page of sheet “G” is filled out for each.

- Sheet "E" indicates the share of the authorized capital of each member of the company.

- Sheet "G" contains information about an individual who has the right to act without a power of attorney on behalf of the company. If there are several such persons, then a separate page is filled out for each.

- Sheet "K" indicates the codes of economic activity.

- The final sheet "O" is filled in in the presence of a notary. This is where the applicant's signature is recorded.

The decision to carry out the reorganization by spin-off is drawn up in an arbitrary form in the form of an extract from the minutes of the general meeting or as a decision of the sole participant.

The decision to reorganize by spin-off in case of voting by several participants is taken only unanimously.

For clearance letter of guarantee there is no single stencil. The letter is drawn up in any form, but on letterhead. In this letter, you must specify the details of the landlord, as well as the address of the premises and its area.

The letter of guarantee must contain detailed information about the lessor and a mandatory indication of his ownership

A company reorganized as a result of separation of an enterprise from it submits the following set of documents:

- an application in the form P13001 for a decrease in the authorized capital;

- an application in form P14001 for a reduction in the nominal value of the participants' shares;

- document confirming the payment of the state fee;

- amended charter;

- decision or protocol on amendments to the articles of association.

Form P14001 is a very cumbersome document. It includes over fifty pages. However, in the case of distribution of a share between the participants of the company, only the following are filled in this form:

- First (title) page.

- Sheets "D", "C" and "D", containing data on the participants in the company. "D" is filled in individuals. "B" - for resident legal entities. "G" - for foreign legal entities.

- Sheet "З", in which information is filled in on the transfer of the share to the company and its distribution among the remaining participants.

- Sheet "P", which contains information about the applicant.

Both packages of documents are sent to the tax office at the same time.

The final stage

This stage begins with the transfer of documents to the tax office and ends with the transfer to the applicants of a package of documents confirming the changes made. According to the law, five days are allotted for processing the received documents by the tax inspectorate.

After processing the submitted documents, the IFTS makes appropriate changes to the single register legal entities (USRLE). Then she hands over to the representatives of the reorganized LLC and the newly created company all registration documents. If after a five-day period the documents were not requested, then they are automatically sent by mail to the specified legal addresses.

The following documents are issued to the company reorganized as a result of separation:

- record sheet of the Unified State Register of Legal Entities;

- the charter of the LLC (one copy) with the mark of the Federal Tax Service.

The society created as a result of the spin-off is given the following package of documents:

- OGRN certificate (main state registration number);

- TIN certificate;

- record sheet of the Unified State Register of Legal Entities;

- charter with a mark and seal of the tax office.

Positive and negative aspects of the reorganization through the allocation

The main advantage of carrying out a reorganization in the form of a spin-off is, of course, the solution to the problems that gave rise to the idea of such a reorganization. Among them:

- optimization of arisen debts;

- the emergence of new areas of activity that require specialization;

- expansion of activities, leading to cumbersomeness and difficulties in managing an expanded enterprise;

- disputes between owners.

However, the extraction process also entails certain risks. The main risk arises from the fact that, by carrying out the reorganization, the company thereby attracts the close attention of both tax authorities and creditors. The latter may, relying on the provisions of Art. 60 of the Civil Code of the Russian Federation, to demand early payment of debts. At the same time, creditors, in order to return their money, have the right to be held jointly and severally liable:

- reorganized (parent) enterprise;

- newly created company;

- responsible executors of reorganization.

In the event of a delay in repayment of loans, not only the reorganized and emerging enterprises, but also the founders of these organizations will be found guilty.

After the reorganization, creditors may also demand the repayment of debt obligations in court. The reason for such an appeal may arise if the amount of net assets of the reorganized company becomes less than the amount of the authorized capital. Then the creditors may claim that the reorganization was deliberately aimed at harming their financial interests. And in this case, not only the reorganized company, but also the newly created enterprise can be held liable.

Such actions of creditors, both at the stage of reorganization and after it, will certainly attract the attention of the tax authorities. And although it is not mandatory to conduct tax audits during a spin-off reorganization, claims by creditors will provide a legitimate reason for conducting audits. Therefore, a careful analysis of the positive aspects and risks that may arise from the reorganization by spin-off is required.

Video: How to choose the right selection reorganization option

Reorganization in the form of separation requires a complex and lengthy procedure involving experts in the field of economics, finance, accounting and law. A thorough and professional approach is needed to all stages of this process: from preparing an extraordinary general meeting to amending the constituent documents of a reorganized company and registering a new enterprise.

Many companies come to a dead end, when development stops, work begins to make a loss, and the team does not function effectively. by the most common solution such a problem is his work. There are several options for this procedure. One of them is selection.

What is spin-off reorganization

Concept and essence

This type of restructuring of the company implies the creation of a new organization on the basis of / from a part of the old organization, that is, the allocation of a new enterprise. It is important that the new can only be of the same organizational and legal form. In such a process, part of the assets is transferred, as well as the responsibilities of the soil company. The reorganized company, as a rule, also remains in operation.

If we talk about the reasons causing the need for reformatting, then often it becomes the threat of the complete disappearance of the company. As already indicated, the new legal entity takes over part of the assets and obligations of the old organization, but is not responsible and does not share the amount of taxes, debts and loans due to the parent company.

However, if the old company is unable to fully recover, the new legal entity may be required by court order to share fines, taxes and other payments with the enterprise. However, such cases are rare, as it is quite difficult to achieve such a court decision.

What is reorganization in the form of allocation, this video will tell:

Regulatory regulation

Such global changes in the organization are regulated by several laws. Two main legal act this is:

- Federal Law “On Limited Liability Companies” dated February 8, 1998. Amended on July 29, 2017. The reorganization is described in Article 55, “Spin-off of Companies”.

- Article 57 on the reorganization of legal entities of the "Civil Code" of November 30, 1994. Edition July 29, 2017.

Pros and cons

Reorganization by allocation has both pluses and minuses. From positive sides is the prevention of bankruptcy, a new chance for the productive functioning of the company, a “clean” tax, credit, penalty history.

However, the last point may create difficulties for a young entity. There are cases when law enforcement officers suspect organizations of bad faith, namely, reorganization in order to avoid paying taxes or at least reduce the amount of mandatory payments, and not to conduct production activities.

If the fact of such a scheme is revealed and the allocation has taken place in order to prevent the excess of the income limit, the tax liability of the corporation is recalculated.

When a reorganization in the form of a spin-off is carried out by a production that has, the following scheme often occurs: all the assets of the old organization are transferred to the new one, after which the first one declares bankruptcy and does not pay the outstanding loan. The main feature of such a scheme is the transfer of most of the enterprise's funds to a new legal entity.

If the reorganization is honest and does not aim to avoid paying debts, the organization intending to carry out the spin-off must publish an official statement in the State Registration Bulletin.

Kinds

Reorganization by allocation can have several options for the end result.

- Most often, a separate, independent enterprise is created.

- However, there are times when a block of a corporation splits off in order to another similar organization. The second scenario is typical for cases when the company's management has disagreements or it was decided to retrain, change the direction of work, and the allocated part became unprofitable or useless.

Reorganization by allocation is possible in two ways, as this video will explain:

Process

The reorganization process is a rather long procedure that requires time, knowledge and accuracy.

The first stage is at which the question of reformatting by highlighting is raised, and appropriate decisions are made. To approve the decision, a majority of votes is required: three-quarters "for" the shareholders and owners present at the meeting. If the owner of the shares is unable to attend the meeting, he/she has the opportunity to fill out a voting ballot earlier and return it no later than 2 days before the meeting.

- Process and conditions of reorganization;

- Procedure for the exchange and division of shares (for joint-stock companies);

- Person Information CEO or another leader for; Details of the two bodies, the board of directors and the supervisory board for the new legal entity.

- Charter of the new enterprise;

- and its copy.

Partition balance

Another mandatory aspect that the parent company must approve after voting is the separation balance sheet for which a part of the funds is transferred to the new person. As a rule, the new firm receives a smaller part of the assets. It is important that the separation balance sheet should include information about the division of taxes and loans (if any), division and property.

To create a new enterprise, the following documents are required:

- registration statement,

- tax registration,

- as well as copies of passports of leaders.

Separation balance sheet example

The reorganization of an LLC in the form of a spin-off is a set of measures aimed at the formation of one or more organizations on the basis of succession, but unlike other types of reorganization, the liquidation of the company does not occur (it continues to exist). The need to implement such a task may arise when creating a common company, expanding a business, or acquiring another LLC that has financial difficulties. What reorganization options are there? What are the features of performing this procedure in the form of selection? What are the milestones for 2018? Let's consider these points in more detail.

Types and features of reorganization

In the legislation of the Russian Federation, there are six forms of reorganization of an LLC:

- merger. In this case, a new legal entity is formed, which assumes the rights and obligations of the companies participating in the procedure. After the completion of the process, the "smaller" participants cease to exist, and information about them is removed from the Unified State Register of Legal Entities. This form of reorganization is suitable for the liquidation of the company.

- transformation. The peculiarity of the reorganization is that the LLC changes its organizational and legal form. After completion of all procedures, it becomes a CJSC, that is, a closed joint stock company.

- Selection. The main difference is the preservation of the company, which acts as a donor. This liquidation option is suitable for cases where there are several owners in the company, and the existence of disagreements does not allow them to conduct a joint business.

- Separation- reorganization, after which several individual companies are formed, endowed with their own rights and obligations. As soon as the process is completed, the donor ceases to exist, and information about him is excluded from the Unified State Register of Legal Entities.

- Accession. In this case, a group of legal entities are combined into one company. The option is used in the process of absorption by a large company of smaller LLCs, as well as in the case of a group of enterprises merging into one holding company. All obligations and rights are transferred to the operating company.

- Combined method. This reorganization combines various ways- separation, separation, merger and accession.

General algorithm of actions

The reorganization of the company, regardless of the chosen method, takes place in several stages:

- Decision-making.

- Informing the registration authority about the start of the process.

- Entering a mark on the launch of the reorganization of the company in the Unified State Register of Legal Entities.

- Print ads in the media. At this stage, information about the participants in the process, terms, as well as data on the procedure for submitting claims should be indicated.

- Informing creditors by each of the participants in the process.

- Transfer of securities for the reorganization of the company.

- Obtaining ready-made documents that should confirm the completion of the reorganization.

It was noted above that the separation implies the creation of one or a group of LLCs with the subsequent transfer of the rights and obligations of the company (the one that is subject to reorganization) to it. This form of transformation is often used to liquidate an LLC.

Reorganization by spin-off can be done for the following reasons:

Reorganization by spin-off can be done for the following reasons:

- The founders of the company cannot find a common language and see further development in different ways.

- There was a need for the financial recovery of LLC by separating unprofitable forms of activity.

Step-by-step instruction

Reorganization in the allocation process takes place in several stages:

- Holding a general meeting and making an appropriate decision. This step is the most important in the matter of reorganization by spin-off. Here it is required to gather the founders of the society and raise the issue of its reorganization. Depending on the number of participants, a meeting can be attended by one or more people. The result of the meeting is the drawing up of minutes (decisions). In the process of discussing the situation, the following issues are considered - the conditions for the allocation of a new company, the procedure for implementing this task, the number of participants in the new LLC, and so on. You can start the procedure only if there are votes.

- Inventory. The next step is to assess the value of the property that is at the disposal of the company. This procedure is mandatory in the extraction process.

- Creation of a separation balance sheet - accounting paper, thanks to which a division is made between the reorganized and the spin-off company. Special attention is paid to rights, finances and assets.

- Making an application. As soon as the procedures discussed above are completed, you can proceed to the execution of the application and its transfer to the Federal Tax Service and registration structures. This is required to inform the authorized bodies about the upcoming transformation. According to the legislation, the document is required to be certified by a notary, and then sent to the authorized body. Three days are given to provide a response. The key points in the statement are the first and fourth. In the first one, it is required to indicate the number of persons participating in the procedure. If the subsidiary has not yet been formed, one person must be indicated. Item number four indicates the final number of companies that will appear after the reorganization. It depends on how many divisions will be made.

- Informing creditors. After registration of the reorganization in the Unified State Register of Legal Entities, creditors must be notified. This will take up to five days. In order to have evidence of data transfer on hand, it is recommended that notification be made by registered letter (subject to notification). In this case, a mandatory condition is an inventory of the transferred documents.

- As soon as the information is entered into the register, it is required to report the changes made to the State Registration Bulletin. The work is done twice a month. The announcement itself must be published within 2 months.

- Approval of the articles of association for each newly formed company. At the same stage, governing bodies are appointed.

- State registration of newly formed LLCs. Here, amendments are also made to the statutory papers.

- Informing about the reorganization of off-budget funds.

At the final stage, it remains to receive statistical codes, print and open a current account. The extraction process takes a period of 2 to 3 months. From the moment of state registration of the separated legal entities, the procedure is considered completed.

It is worth considering that the reorganization of a company through a spin-off can be complicated by a number of problems associated with litigation.

The latter may arise from the division of debt or property between creditors. In some cases, there is forced allocation through the courts after filing statement of claim antitrust authority.

What documents are required?

To carry out the reorganization by type of allocation, it is necessary to prepare the following package of papers:

To carry out the reorganization by type of allocation, it is necessary to prepare the following package of papers:

- Application (issued in the form P12001). It should contain information about the LLC, which will appear after the completion of the procedure, the number of founders who will work in new organization, as well as the number of participants participating in the procedure.

- Protocol (decision) on the allocation of a new LLC.

- A legal act of a newly formed company that appeared after the completion of the transformation.

- Decision to appoint a new body responsible for the charter.

- Separation balance sheet of the new branch.

- Receipt confirming the payment of state duty.

- Newsletter pages proving the fact that the company informed about decision(enough copies).

- Postal receipt confirming that messages have been sent to creditors.

- A message from the Pension Fund of the Russian Federation that the organization has no debt. Under the law, this certificate is not necessary, but in practice its presence can significantly speed up the process.

As soon as all the papers are collected, the owner of the LLC transfers them to the registering structure. Further government agency 5 days are given to process the received information and transfer two packages of documents. One is for the newly registered company, and the other is for the main LLC. The exact date when the processing will be completed is noted in the receipt (issued to the owner at the time of transfer of documents). If the manager cannot pick up the papers on his own, he has the right to get the job done by a trusted person or request that it be sent to the company's address. In the first case, a notarized power of attorney is required.

The subtleties of real estate transition

In order for the new company to secure the rights to existing real estate, it is required to collect and transfer the following papers:

- Protocol (decision) on reorganization.

- Dividing balance sheet of LLC.

- The act of acceptance and transfer, which is drawn up in relation to the property transferred to the new company.

- Papers securing the company's rights to real estate.

- The main documents of the newly formed division. To carry out the reorganization, it is necessary to apply to the authorized body with a data package, as well as a receipt for payment of the state duty.

When reorganizing an LLC through a spin-off, you should pay attention to the tax consequences. So, if the primary company, after the completion of the process, cannot fulfill its obligations to the Federal Tax Service, you can run into trouble. In the event that the inspectors, and subsequently the court, confirm that the reorganization was carried out for tax evasion, the spun-off companies will have to pay off their own funds.

For beginners: breeding a broiler at home Boiled water for broilers

Only lovers will survive

Features of advertising aimed at children

retouching old photos in photoshop retouching old photos

What is an NPO: decoding, definition of goals, types of activities Does a non-profit organization have the right