DEFINITION

Operating lever(operating or production leverage) - an indicator that reflects the excess of the growth rate of profit over the growth rate of the company's revenue.

The purpose of the functioning of any company is to increase profits from sales, including net profit, which should be aimed at maximizing productivity and growth financial efficiency(value) of the enterprise.

The operating leverage formula gives you the ability to manage sales profits in the future by planning revenue in the future.

The main factors affecting revenue volumes are:

- product prices,

- Variable costs, which change depending on changes in the volume of production;

- Fixed costs that do not depend on production volumes.

The goal of any enterprise is to optimize variable and fixed costs, adjust the pricing policy, thereby increasing the profit from the sale.

Leverage Formula

The methodology for calculating the operating leverage formula is as follows:

OR \u003d (V - Per.Z) / (V - Per.Z - Constant.Z)

OR \u003d (V - Lane. Z) / P

OR=VM/P=(P+Cons.Z)/P=1+(Cons.Z/P)

Here OR is an indicator of operating leverage,

B is the revenue

Per.Z - variable costs,

Post.Z - fixed costs,

P - the amount of profit,

VM - gross margin

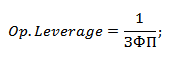

Operational leverage and financial safety margin

The indicator of operating leverage is directly related to the margin of financial safety through the ratio:

RR = 1/FFP

Here OP is the operating lever,

ZFP - a margin of financial strength.

With an increase in the operating leverage, the company's financial strength decreases, which contributes to its approaching the threshold of profitability. In this situation, the company is not able to ensure sustainable financial development. To prevent this situation, it is recommended to constantly monitor production risks and their impact on financial performance.

What does the operating lever show

The operating lever can be of two types:

- Price operating leverage that reflects price risk (the impact of price changes on profit margins);

- Natural operating leverage is the production risk or the dependence of profit on output.

The high value of the operating leverage indicator reflects a significant excess of revenue over profit, which indicates an increase in constant and variable costs.

The increase in costs is due to the following reasons:

- Modernization of used capacities, increase in production areas, increase in the number of production workers, introduction of innovations and improvement of technologies.

- Minimization of product prices, low effective growth wage costs for low-skilled personnel, an increase in the number of defective products, a decrease in the efficiency of production lines, etc.

Thus, all production costs can be effective, which increase the production and scientific and technological potential, as well as inefficient, which hinder the development of the enterprise.

Examples of problem solving

EXAMPLE 1

Leverage (from the English leverage - the action of the lever).

Production (operating) leverage - the ratio of fixed and variable costs of the company and this ratio to the operating, that is, before interest and taxes. If the share of fixed costs is high, then the company has a high level of production leverage, while a small amount of production can lead to significant change operating profit.

The action of the operational (production, economic) lever is manifested in the fact that any change in sales proceeds always generates a stronger change in profit.

Production leverage effect (EPR):

EPR = VM / BP

VM - gross marginal income;

BP - balance sheet profit.

That. operating leverage shows how much the company's balance sheet profit changes when revenue changes by 1 percent.

The operating lever indicates the level of entrepreneurial risk of a given enterprise: the greater the impact of the production lever, the higher the degree of entrepreneurial risk.

Financial (credit) leverage - the ratio of borrowed capital and equity capital of the company and the impact of this ratio on net profit. The higher the share of borrowed capital, the lower the net profit, due to the increase in interest costs.

The size of the ratio of borrowed capital to equity characterizes the degree of risk, financial stability. A highly leveraged company is called a financially dependent company. A company that finances its own with only its own capital is called a financially independent company.

The cost of borrowed capital is usually less than the additional profit it provides. This additional profit is added to the return on equity, which allows you to increase the profitability ratio. That. there is an increase in the return on equity, obtained through the use of credit, despite the payment of the latter.

It can only occur if the trader uses borrowed funds.

Effect of financial leverage (EFF), %:

EGF \u003d (1 - C N) * (R A - C ZK) * ZK / SK

where:

1 - C N - tax corrector

R A - C ZK - differential

ZK / SK - lever arm

C N - income tax rate, in decimal terms;

R A - return on assets (or return on assets ratio = the ratio of gross profit to the average value of assets),%;

CZK - the price of borrowed capital of assets, or the average interest rate for a loan, %. (for a more accurate calculation, you can take the weighted average rate for the loan)

ZK - the average amount of borrowed capital used;

SC - the average amount of equity capital.

- The effectiveness of the use of borrowed capital depends on the ratio between the return on assets and the interest rate for the loan. If the rate for a loan is higher than the return on assets, the use of borrowed capital is unprofitable.

- Ceteris paribus, greater financial leverage produces greater effect.

Associated lever. As the impact of operating and financial leverage increases simultaneously, less and less significant changes in the physical volume of sales and revenue lead to more and more large-scale changes in net profit. This thesis is expressed in the formula for the conjugate effect of operational and financial leverage:

P \u003d EGF * EPR

P is the level of the conjugated effect of operational and financial leverage.

The formula for the conjugate effect of production and financial leverage can be used to assess the total level of risk associated with the enterprise, and determine the role of entrepreneurial and financial risks in shaping the total level of risk.

We will analyze the operating lever of an enterprise and its impact on production and economic activities, consider the formulas for calculating the price and natural leverage and analyze its assessment using an example.

Operating lever. Definition

Operating lever (operating leverage, production leverage) - shows the excess of the growth rate of profit from sales over the growth rate of the company's revenue. The purpose of the functioning of any enterprise is to increase profits from sales and, accordingly, net profit, which can be directed to increasing the productivity of the enterprise and increasing its financial efficiency (value). The use of operating leverage allows you to manage the future profit from the sales of the enterprise by planning future revenue. The main factors that affect the amount of revenue are: product price, variable, fixed costs. Therefore, the goal of management becomes the optimization of variables and fixed costs, regulation pricing policy to increase sales revenue.

Formula for calculating price and natural operating leverage

|

Formula for calculating price operating leverage |

The formula for calculating natural operating leverage |

where: Op. leverage p - price operating leverage; Revenue - sales revenue; Net Sales - sales profit (operating profit); TVC (Total variable Costs)

– total variable costs; TFC (Total Fixed Costs) where: Op. leverage p - price operating leverage; Revenue - sales revenue; Net Sales - sales profit (operating profit); TVC (Total variable Costs)

– total variable costs; TFC (Total Fixed Costs)

|

where: Op. leverage n - natural operating leverage; Revenue - sales revenue; Net Sales - sales profit (operating profit); TFC (Total Fixed Costs) - total fixed costs. |

What does the operating lever show?

Price operating leverage reflects price risk, that is, the impact of price changes on the amount of profit from sales. shows the production risk, that is, the variability of profit from sales depending on the volume of output.

High operating leverage reflects a significant excess of revenue over sales profit and indicates an increase in fixed and variable costs. The increase in costs may be due to:

- Modernization of existing facilities, expansion of production facilities, increase production staff, introduction of innovations and new technologies.

- Decrease in sales prices of products, inefficient growth in the cost of wages for low-skilled personnel, an increase in the number of defects, a decrease in the efficiency of the production line, etc. This leads to an inability to provide the necessary sales volume and, as a result, reduces the margin of financial safety.

In other words, any costs at the enterprise can be both effective, increasing the production, scientific, technological potential of the enterprise, and vice versa, hindering development.

Operating leverage. How does productivity affect profits?

Operating leverage effect

Operational (production) effect leverage lies in the fact that a change in the company's revenue has a stronger impact on sales profit.

As we can see from the above table, the main factors affecting the size of the operating leverage are variable, fixed costs, and also profit from sales. Let's take a closer look at these leverage factors.

fixed costs- these are costs that do not depend on the volume of production and sale of goods, they, in practice, include: rent for production areas, wage management personnel, loan interest, unified social tax deductions, depreciation, property taxes, etc.

Variable costs - these are costs that vary depending on the volume of production and sale of goods, they include the costs of: materials, components, raw materials, fuel, etc.

Revenue from sales depends primarily on the volume of sales and the pricing policy of the enterprise.

Operational leverage of the enterprise and financial risks

The operating leverage is directly related to the financial strength of the enterprise through the ratio:

Op. Leverage - operating leverage;

ZPF - a margin of financial strength.

With the growth of the operating leverage, the financial strength of the enterprise decreases, which brings it closer to the threshold of profitability and inability to ensure sustainable financial development. Therefore, the company needs to constantly monitor its production risks and their financial impact.

Consider an example of calculating the operating leverage in Excel. To do this, you need to know the following parameters: revenue, profit from sales, fixed and variable costs. As a result, the formula for calculating the price and natural operating leverage will be as follows:

Price operating leverage=B4/B5

Natural operating lever=(B6+B5)/B5

Example of calculating operating leverage in Excel

Based on the price leverage, it is possible to evaluate the impact of the company's pricing policy on the amount of profit from sales, so if the price of products increases by 2%, the profit from sales will increase by 10%. And with an increase in production volumes by 2%, the profit from sales will increase by 3.5%. Similarly, the opposite is true, with a decrease in price and volume, the resulting value of profit from sales will decrease in accordance with the leverage.

Summary

In this article, we examined the operating (production) lever, which allows us to evaluate the profit from sales, depending on the pricing and production policy of the enterprise. High leverage values increase the risk of a sharp reduction in the company's profits in an unfavorable economic situation, which, as a result, can bring the company closer to the break-even point, when profits equal losses.

When compiling a budget, it is worthwhile to figure out how the company's profit is dependent on its revenue, how it will change with an increase or decrease in sales. key indicator, allowing to make such a forecast, is the operating (production) lever.

Important in the article:

- Operating lever. Calculation formula

- Calculation of the production leverage (operating leverage)

- Manufacturing Lever

How to Calculate Operating Leverage

Formula. Calculation of the production leverage (operating leverage)

For example, a leverage value of 10 percent indicates that profits increase or decrease by that many percent when sales revenue increases or decreases by 1 percent. The higher the production leverage, the faster the company increases profits.

What affects the level of production leverage (leverage)

The production leverage (leverage) depends on - ratio. The more fixed costs in the company's expenses, the higher it is. Accordingly, companies with low production leverage are dominated by variable costs (how to quickly analyze costs, see).

It is worth noting that this indicator characterizes, on the one hand, the possible growth rate of profit, on the other hand, the rate of its decline. At , a company with a large value of production leverage (a high share) will be able to increase profits faster than a company with a low level of this indicator. But in the reverse situation, when the first company falls, it will lose profits at a much greater rate. The higher the production lever, the stronger the company's dependence on the volume of sales of products (how to determine the critical point, see).

What level of production leverage is optimal for the company

To figure out what value of the production lever you need to strive for - high or low, you have to form a forecast for the company's future sales volumes (see how to do this).

With a high risk of falling sales, low production leverage (in other words, a low share of fixed costs) is beneficial, since with a reduction in sales, it is necessary to solve the problem of minimizing profit losses. And vice versa, with favorable market conditions, growth in sales volumes, a high leverage is beneficial (in other words, a high share of fixed, low share of variable costs). This cost structure contributes to profit maximization.

How to optimize production leverage

Timely, that is, the ratio of variable and fixed costs, will help to correctly manage the production lever of the company. At the same time, it is necessary to study each one in detail and evaluate it from the point of view of dependence on the volume of sales (how to evaluate their impact on the cost price, see Fig.

Leverage is the sensitivity of a firm's income to changes in sales. In other words, leverage are elasticities that relate the change in one item of income when another item changes.

The income of a business can be measured before and after taxes.

Distinguish:

- operating lever

- financial leverage

- combination lever

Production (operational) leverage. The ratio of a company's fixed to variable costs and the impact of this ratio on operating profit, that is, earnings before interest and taxes. If the share of fixed costs is large, then the company has a high level of production leverage. And even a small change in production volumes can lead to a significant change in operating profit.

Operating lever - quantification changes in profit depending on changes in sales volumes.

Operating leverage effect-- an expression of the fact that any change in sales revenue generates a change in profits. The strength of operating leverage is calculated as the quotient of sales revenue after recovering variable costs to earnings.

Production leverage effect(EPR) shows the degree of sensitivity of profit from sales to changes in sales proceeds. The value of EPR increases enormously with a fall in production and its approach to the threshold of profitability, at which the enterprise operates without profit. That is, under these conditions, a small increase in sales proceeds generates a multiple increase in profits, and vice versa.

Financial leverage (financial leverage) is the ratio of the company's borrowed capital to its own funds, it characterizes the stability of the company. The smaller the financial leverage, the more stable the position. On the other hand, borrowed capital allows you to increase the return on equity, i.e. earn additional return on equity.

The indicator reflecting the level of additional profit when using borrowed capital is called effect of financial leverage. It is calculated using the following formula:

EGF \u003d (1 - Sn) H (KR - Sk) H ZK / SK,

EGF -- the effect of financial leverage,%.

Сн - income tax rate, in decimal terms.

KR -- return on assets (the ratio of gross profit to the average value of assets),%.

Sk -- the average interest rate for a loan,%. For a more accurate calculation, you can take the weighted average rate for the loan.

ZK -- the average amount of borrowed capital used.

SC -- the average amount of equity capital.

The effect of financial leverage is an increment to the return on equity, obtained through the use of borrowed money despite their fees.

Financial leverage shows the impact of financial costs associated with borrowing capital on the amount of net profit. If it is a positive value, then it increases the return on equity. Positive financial leverage will be provided that the economic profitability of capital is higher than the loan interest rate. In a market economy, the loan interest rate is determined, apart from all other conditions, by the amount of borrowed capital; the higher the amount of borrowed capital in the structure of the sources of funds of the enterprise, the higher the loan interest rate and the lower the net profit and, accordingly, the return on equity. The use of net income for consumption increases the company's need for borrowed capital. With a high price of resources and low return on assets, this leads to a negative effect of financial leverage and a decrease in the return on equity, which limits the internal growth rate of the enterprise.

An analysis of the use of profits reveals how efficiently funds were allocated for accumulation and consumption. Here are the following evaluation criteria:

- 1) if the share of borrowed funds in the capital structure increased, then social payments limited internal growth rates;

- 2) if the internal growth rates increase, then the profit distribution policy is chosen correctly.

Evaluation of the effectiveness of the distribution of profits for accumulation and consumption is also carried out using a quantitative measurement of the effect of financial leverage.

Analysis of the profit remaining at the disposal of the enterprise involves the solution of the following tasks:

- Quantitative assessment of the influence of factors on the change in net profit;

- Identification of trends that have developed in the distribution of profits for the reporting period;

- assessment of the impact of profit distribution on the financial condition of the enterprise;

- · measuring the influence of factors on the value of special funds;

- · Evaluation of the effectiveness of the use of accumulation and consumption funds in accordance with the performance indicators of the economic potential.

Aggregate combined lever

Together, the working capital and financial leverage are combined lever and show how net income will change depending on the relative change in sales volume. The combined lever is found as the product of the turnover and financial levers.

For beginners: breeding a broiler at home Boiled water for broilers

Only lovers will survive

Features of advertising aimed at children

retouching old photos in photoshop retouching old photos

What is an NPO: decoding, definition of goals, types of activities Does a non-profit organization have the right